In economics, the concepts of demand and supply are fundamental in determining the prices of goods and services in a market economy. These forces shape how resources are allocated and how products are distributed across consumers. Demand and supply interact to establish equilibrium prices, which in turn influence both consumers' purchasing decisions and producers' production choices. Understanding how demand and supply work is essential for comprehending market behavior, price fluctuations, and the factors that drive economic decisions in both individual and collective contexts. This article explores the concepts of demand and supply, how they interact to affect prices, and how they influence decisions made by consumers and producers.

Demand refers to the quantity of a good or service that consumers are willing and able to purchase at various prices, over a specified period of time. The law of demand states that, all else being equal, as the price of a good or service decreases, the quantity demanded by consumers increases, and conversely, as the price increases, the quantity demanded decreases. This inverse relationship between price and demand is central to understanding consumer behavior in the marketplace.

The law of demand is one of the fundamental principles of economics. It suggests that consumers tend to purchase more of a good or service when its price falls, and less when its price rises. This is because lower prices make goods and services more affordable, and consumers are more likely to buy more as the perceived value increases.

Supply refers to the quantity of a good or service that producers are willing and able to offer for sale at various prices, over a specified period of time. The law of supply states that, all else being equal, as the price of a good or service increases, the quantity supplied by producers increases. Conversely, as the price decreases, the quantity supplied decreases. This direct relationship between price and supply is central to understanding how producers respond to market incentives.

The law of supply suggests that producers are willing to produce and sell more of a good when its price is high, because they can earn more revenue. Conversely, when the price falls, the incentive to produce decreases, and suppliers are less willing to offer the good at lower prices.

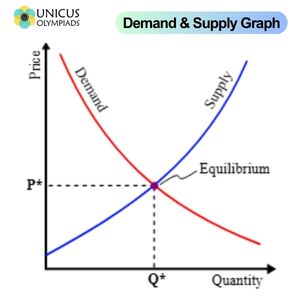

Demand and supply interact in the market to determine the equilibrium price—the price at which the quantity demanded by consumers equals the quantity supplied by producers. The market reaches an equilibrium when there is no excess demand (shortage) or excess supply (surplus). Changes in either demand or supply can shift the equilibrium price and quantity.

At the equilibrium point, the amount of a good or service that consumers are willing to buy matches the amount that producers are willing to sell. This price is known as the equilibrium price, and the quantity exchanged is the equilibrium quantity.

Changes in factors that affect demand or supply can lead to shifts in the demand curve or supply curve, altering the equilibrium price and quantity. A shift in the demand curve indicates a change in the quantity demanded at every price, while a shift in the supply curve indicates a change in the quantity supplied at every price.

Prices act as signals in the market, guiding both producers and consumers in their decision-making. Prices reflect the relative scarcity or abundance of a good or service and incentivize production and consumption accordingly. They help allocate resources efficiently by directing them to where they are most valued.

For consumers, prices influence their purchasing decisions. When prices are high, consumers may reduce their demand for certain goods, choosing to spend their money on other items or delaying purchases. Conversely, when prices are low, consumers may increase their demand for goods and services. In this way, prices guide consumer behavior and help ensure that limited resources are allocated according to consumer preferences.

For producers, prices determine the profitability of producing goods. High prices signal that a good is in demand, encouraging producers to increase production. Low prices, however, may discourage production, leading to reduced supply. Producers also consider input costs, technology, and regulations when making production decisions, but prices are a key factor in determining whether producing a good is financially viable.

Understanding demand and supply is critical for both consumers and producers in the real world. Many industries rely on these concepts to determine pricing strategies, forecast demand, and optimize production.

In the housing market, the interaction of demand and supply determines property prices. When demand for homes rises due to factors like population growth or low interest rates, housing prices increase. On the other hand, when supply increases due to new construction or a decrease in demand due to higher interest rates, prices may fall.

The technology market provides another example of demand and supply. High demand for new smartphones, for example, drives up prices, especially when supply is limited due to production constraints. However, as production increases or demand decreases over time, the price may stabilize or decrease as newer models are released.